Here’s a playbook to manage it: The “Outside-In, Bottom-up” framework for successful AI transformation.

AI moves at 100. People adapt at 10. The Fortune 500 adopts at 1.

That ratio between the velocity of machine intelligence and the metabolic rate of the Fortune 500 is the most consequential mismatch in modern business. This is not a technology-adoption problem. It is a problem of institutional physics: large companies engineered for predictability, quarterly cadence, and hierarchical control were not made to absorb a force that doubles in capability every few months, and they will not spontaneously reconfigure themselves on its schedule.

Nobody designed the Fortune 500 for this. And the enterprise, function by function, is beginning to melt under the heat of AI.

Here’s the simplest way I can put it: when lead melts, the substance remains but the rules change. It moves faster, fills new shapes, and the old container can’t hold it. That is what AI is doing to knowledge work. The work hasn’t disappeared, it has changed state. But every org chart, approval chain, and talent model in the Fortune 500 was built to hold the solid.

The only question for current leadership is whether they manage the transition on their terms, or have it imposed on someone else’s. And if it’s the former, the best approach is the “Outside-in, Bottoms-up” playbook for AI adoption.

GenAI: The Mother of 1,000-yard stares

A new model drops. A benchmark crumbles. An automation is launched that does in 45 seconds what a team of 12 once did in a week. Once the realization sinks in, you stare out the window. But the focus of that thousand-yard stare keeps changing:

· 2024 (The Model Era): “How does that job survive?”

· 2025 (The Agentic Era): “How does that department survive?”

· 2026 (The Automation Era): “How does that company survive?”

Each question is broader than the last, and none of them has a comfortable answer. The escalation itself is the message.

But then you go to the next Zoom meeting, and the discussions are refreshingly familiar: budget reviews, sales forecasting, customer meetings, preparing for the next offsite. And you say “This is fine.”

But it’s not fine. Not even close.

Some take comfort in drawing parallels to the prior technology shifts. Client/Server gave enterprises new plumbing. The Internet gave new distribution. Digital gave new interfaces. But here is the critical distinction: all three of those waves were designed to support a pre-existing industrial structure, with its workers continuing to do the same work. Finance people still did finance. Marketers still marketed. Operators operated. Sellers sold. Coders coded. Designers designed. The technology supported the work; it did not recompose it. Consider the proof: the business model of an EY or an Accenture (the purest knowledge-work scale enterprises on earth) was structurally, financially, and culturally recognizable from 1990 to 2025. Yes, the Internet made for remote and global delivery, but did not change what the work was.

AI changes what work is. It is not a new tool but a new workforce: one that does not sleep, does not negotiate, and improves on a release cycle measured in weeks. And because it addresses the structure of work itself, rather than the tools surrounding it, the entire industrial edifice (e.g., the talent model, the org chart, the assumption that knowledge workers are organized by function and measured by activity) is under intense pressure.

The Melting Point Framework

Every element in nature has a melting point; the temperature at which it transitions from solid to liquid. Ice at 0°C. Lead at 327°C. Iron at 1,538°C. Tungsten holds until 3,422°C.

The analogy maps directly to the enterprise. Every function has its own threshold, the point at which AI makes the existing way of doing the work indefensible. Where the work is primarily digital and cognitive, that point has arrived. Where it demands physical presence, relational trust, or real judgment under ambiguity, it hasn’t…yet. But having watched three technology waves up close, I can tell you: the gap between “not yet” and “too late” has never been shorter.

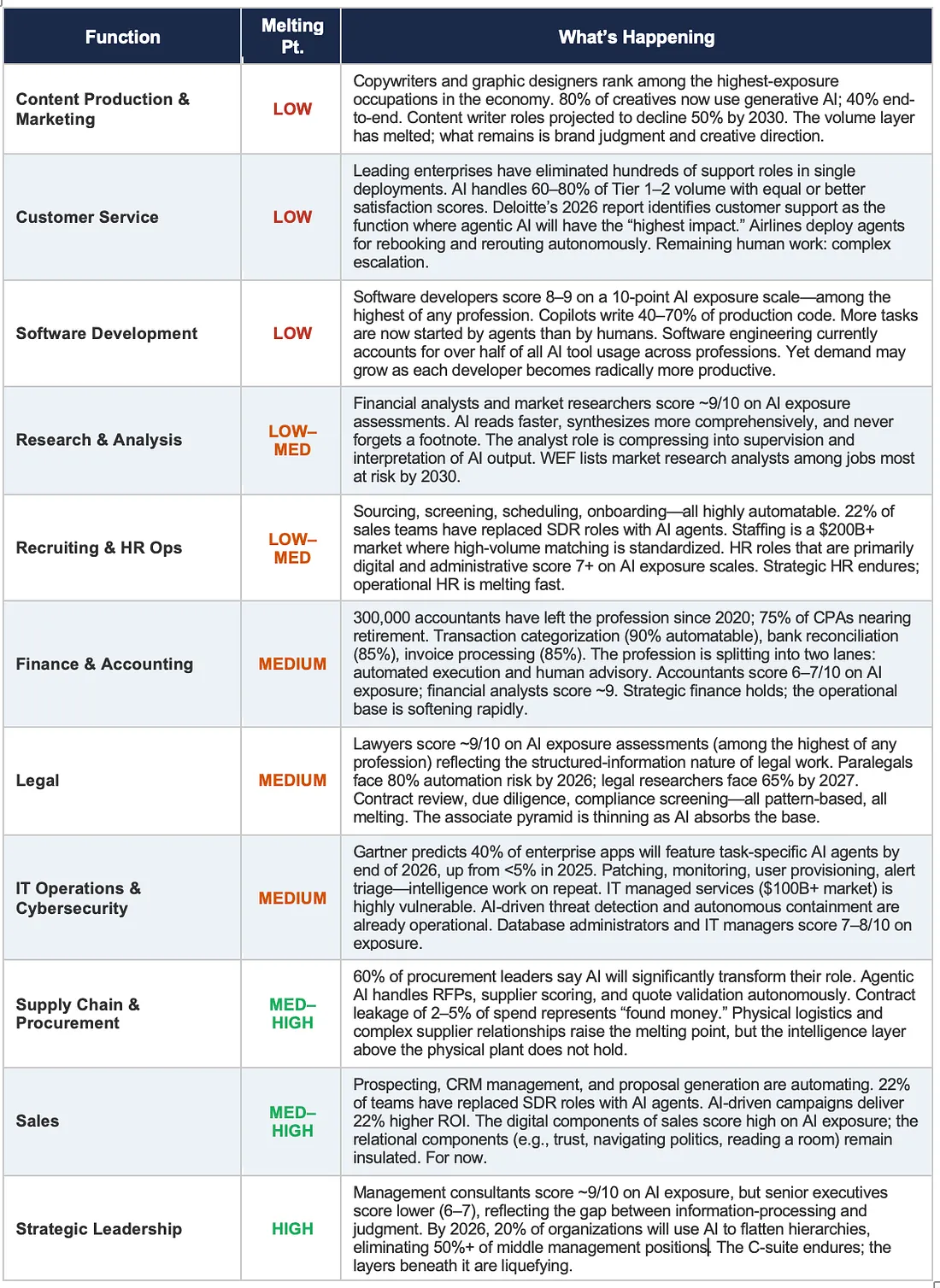

Importantly, the gradient is becoming increasingly specific and predictable. And it is actionable, because it prescribes the order in which an enterprise should move. Disruption cascades from the top of this table downward.

Enterprise Functions, Ranked by AI Melting Point

Many senior executives are in a state of denial over the power of AI. Per the above chart, these leaders (whose own roles carry high melting points) tend to underestimate the urgency of the functions beneath them. That is the trap. But it is also the opportunity: because the melt is now predictable, it can be harnessed.

The recommended approach, and the central argument of this article, is a three-phase sequencing strategy I call the “Outside-in, Bottom-up” playbook.

The Outside-In, Bottom-Up Playbook

Most Enterprise AI strategies fail for the same reason: they start in the wrong place. For example, they launch a center of excellence (rarely central, never excellent). Or appoint an “AI czar” (who reports to the CIO and has no P&L authority), and run proofs of concept (on workflows that are politically safe but economically trivial).

Eighteen months and several million dollars later, they have a portfolio of pilots, a deck for the board, and no institutional muscle.

There is a better way. It follows the melting-point gradient in three phases.

1. Outside-in: automate the work you are already paying other companies to do.

2. Bottom-up: work from the bottom of the Income Statement up, by automating your own lowest melting-point functions in G&A.

3. Cost of Goods Sold: apply the muscle and funding from the first two phases to transform the core of what you deliver to customers.

Each phase teaches the organization something it needs for the next. Skip the sequence, and you will fail at the phase that matters most.

Phase 1 Outside-In: Start with Your Vendors

Here is the move that most executives miss, and that the smartest AI-native startups are already exploiting from the other side of the table: start with the money you are already spending on other people’s employees.

Every Fortune 500 company spends hundreds of millions annually on outsourced services: PR agencies, management consultants, software development shops, design studios, research firms, recruiting firms, legal process outsourcers. These vendors built their business models on the labor arbitrage of the prior era (based on Coasian economics), and their melting points are among the lowest in the enterprise ecosystem. And their invoices are already in your budget.

This is the right starting point for three reasons.

1. The budget already exists. You are not asking the CFO for new money. You are redirecting existing vendor spend (line items that have been in the budget for years) toward AI capabilities that deliver equivalent or better output at a fraction of the cost. A company spending $15 million a year on outsourced research and content production can redeploy $10 million into AI tools and internal orchestration, with the remaining $5 million funding the transition. I have yet to meet a CFO who argues with it.

2. The risk is contained. You are not restructuring your own workforce…yet. You are replacing vendor deliverables: work product that already crosses an organizational boundary, with defined specifications and acceptance criteria. If the AI output falls short, you still have the vendor as a fallback. Critically, from an enterprise change-management perspective, you are sidestepping the two forces that kill most internal AI initiatives: employee resistance and middle-management inertia. Nobody inside the company loses their job in Phase 1. The organizational immune system stays dormant.

3. It builds the institutional muscle you will need for everything that follows. Your teams learn to brief AI agents instead of agencies; to write specifications for machines rather than for account managers. Your procurement function learns to evaluate AI capabilities against outcome benchmarks, not headcount proposals. Your quality assurance processes learn to validate machine output at machine speed. These competencies (what I call AI orchestration) are the precise muscles required for Phase 2 and Phase 3. Without Phase 1, most organizations never develop them.

The targets follow the melting-point table directly. And there is a compounding advantage by starting here. Because Silicon Valley’s current application-level AI investment is disproportionately aimed at exactly these categories (e.g., Anthropic and OpenAI, as well as hundreds of well-funded startups, are building tools that automate precisely the work your vendors do) your company rides a massive R&D tailwind it did not have to fund. Every improvement in the underlying models makes your Phase 1 gains larger, your margins wider, and your internal AI orchestration more sophisticated.

The outsourced perimeter is not just the lowest-risk starting point. It is the highest-leverage one.

The companies that execute Phase 1 decisively can self-fund their entire AI transformation. The ones that protect vendor relationships out of institutional inertia will subsidize someone else’s obsolescent business model while their competitors build internal capability.

Phase 2: Bottoms-Up — Automate Your Own Functions

Once you have built the muscle on external spend, turn it inward. Phase 2 is the automation of your own enterprise functions, starting at the lowest melting points and working upward through the organization.

This is the phase no AI startup can do for you. Startups can sell you tools, and increasingly they can sell you outcomes on outsourced work. But redesigning how your own marketing department, your own finance team, your own recruiters operate? That requires institutional knowledge, organizational authority, and change-management muscle that only the enterprise itself possesses.

This is well-understood ground, and the AI vendor ecosystem is racing to own it. The use cases are converging rapidly across industries because functional work is broadly similar regardless of sector. Marketing is marketing. Recruiting is recruiting. Finance is finance. The automations are arriving fast.

I am seeing it firsthand across every sector I advise:

• Marketing: AI agents generate, test, and optimize campaigns end-to-end, replacing workflows that involved a dozen people across creative, media, and analytics.

• Recruiting: AI screens, matches, schedules, and conducts initial interviews, compressing a four-week hiring cycle to four days.

• Customer service: AI agents handle the majority of inbound volume with equal or better satisfaction scores.

• Finance: AI automates month-end close, variance analysis, and forecasting, work that consumed entire teams for entire weeks.

These are not pilot-stage experiments. They are production deployments at scale, and they share a common feature: the functional melting point was low enough that AI could absorb the volume work while humans shifted to exception-handling and judgment.

Two lessons from Phase 1 prove decisive in Phase 2. First, the self-funding mechanism carries forward. The savings from Phase 1 created an AI investment pool outside the traditional budget cycle; Phase 2 extends that pool as internal automation generates its own returns. The CFO is no longer funding an experiment; she is scaling a model that has already paid for itself. Second, the institutional muscle transfers directly. The teams that learned to brief AI agents on vendor deliverables now know how to decompose an internal function into tasks, allocate those tasks between humans and machines, and validate the output.

Phase 2 also exposes an organizational gap that will otherwise kill the effort. The CHRO owns people but lacks the technical depth to redesign AI-infused workflows. The CIO owns technology but has no mandate for the new talent model. The COO runs today’s revenue engine, which creates built-in bias toward incrementalism. What is missing is an executive who owns work itself: the allocation of tasks across humans and machines and the continuous redesign of that allocation as AI capabilities advance. I have taken to calling this role a Chief Work Officer. Some firms do title this the “Chief AI Officer” (or some derivation). The key point is this executive has to 1.) understand the fundamental units of work by workflow (whether machine or human) and employ first-principles thinking, 2.) know the culture of the firm and enjoy the personal relationships to drive change, 3.) have the authority, the teeth, to get things done. Without it, Phase 2 fragments across silos, and Phase 3 never happens.

Phase 3 The Hard Yards: Cost of Goods Sold (COGS)

Phase 3 is where the most enterprise value is created and destroyed with AI. This is the transformation of what you deliver to your customers: your core products and services, your cost of goods sold, the reason your company exists.

Phase 1 gave you the financial headroom. Phase 2 gave you the organizational muscle: the AI orchestration capability, the governance frameworks, the executive fluency. Phase 3 is where you deploy all of it against your competitive position.

In financial services, it means AI agents that actively manage routine portfolios, generate hyper-personalized financial plans, and surface opportunities the human advisor would have missed, turning a one-to-two-hundred client model into one-to-two-thousand with better outcomes.

In professional services (a space I know well) it means the collapse of the leverage model. Partners selling, managers supervising, associates grinding…that pyramid was designed for an era when volume work required volume humans. When AI absorbs the base, firms that redesign around small senior teams orchestrating AI agents gain a structural cost advantage that competitors simply cannot match.

In healthcare, it means AI that reads imaging, triages patients, monitors chronic conditions in real time, and synthesizes clinical research — fundamentally changing the throughput and quality of care.

In manufacturing, it means supply chains that sense, predict, and adjust in real time. The physical plant has a high melting point; the intelligence layer above it does not. And (finally!) truly smart products which continually adapt to their environment and needs of their users.

Companies that attempt Phase 3 without the institutional muscle built in Phases 1 and 2 will fail. They will launch ambitious pilots, discover they have no AI orchestration capability, no self-funding mechanism, and no muscle memory for human-machine work redesign, and they will retreat to the comfortable incrementalism of bolt-on AI. Their competitors, who followed the sequence, will pull away.

The Thermometer Is Not Waiting

Every element has a melting point. So does every function, vendor relationship and business model. The temperature is rising on a curve that no enterprise controls.

This is not a vendor-selection guide or a technology-adoption roadmap. It is an enterprise transformation framework, and the companies that respect its sequence will build AI capability the way the best organizations have always built capability: progressively, with each phase funding and informing the next. The companies that skip ahead will waste capital and confirm every skeptic’s priors. And the companies that do nothing will discover what the periodic table already knows: when an element reaches its melting point, it does not negotiate. It does not convene a task force. It liquefies.

AI moves at 100. Individuals move at 10. Your company moves at 1.

It’s time to change the math.